You spend $10,000 on accounting software, then spend $120,000 hiring an accountant to use it. The next great company will not sell you software — it will just get your books done. This is not a startup's wishful thinking — it is the core thesis from Sequoia Capital partner Julien Bek's 10,000-word article "Services: The New Software," published in March 2026.

1:6

Software vs. Services Spend Ratio

$1T

Bek's Predicted Next Trillion-Dollar Company

10+

High-Potential Verticals Named

The Core Thesis in One Sentence

If you sell tools, you are racing against the model. If you sell outcomes, every model upgrade makes you faster, cheaper, and harder to replace.

Every AI entrepreneur should print this sentence and tape it to their monitor.

The SaaS paradigm of the past 20 years has been about selling tools: Salesforce sells CRM, HubSpot sells marketing automation, ServiceNow sells IT ticketing. But what users really buy was never the tool itself — they wanted deals closed, customers acquired, problems solved. Tools were just the intermediate step to achieve outcomes. AI's breakthrough is that this intermediate step can be dramatically compressed or even eliminated.

Intelligence vs. Judgement: A Critical Distinction

Bek makes a precise distinction in the article:

| Dimension | Intelligence | Judgement |

|---|---|---|

| Definition | Complex rules, but ultimately rules | Requires experience, taste, and intuition |

| Programming Example | Writing code, running tests, fixing bugs | Deciding what feature to build next |

| Accounting Example | Bookkeeping, reconciliation, report generation | Tax planning, audit judgement |

| AI Capability | Already at human level | Still requires human involvement |

| Business Opportunity | Can be fully automated | Requires human-AI collaboration |

His argument is that writing code is largely Intelligence — rules are complex, but they are ultimately rules. AI can already handle this. But deciding what to build in the next Sprint, whether to take on technical debt, when to ship an imperfect version — that is Judgement, requiring intuition built over years of experience.

The value of this framework is that it tells entrepreneurs where to enter. First capture Intelligence-dense work (many rules, highly repetitive, clear right and wrong), then gradually encroach on the Judgement domain once domain data has been accumulated.

From Copilot to Autopilot: Not an Upgrade, but a Species Leap

The most impactful concept in the article is the leap from Copilot (co-pilot) to Autopilot (self-driving):

This leads to a classic entrepreneur's dilemma:

The Copilot Company's Innovator's Dilemma — your customers are professionals (lawyers, accountants, engineers). If you upgrade from Copilot to Autopilot, you are eating your customers' lunch. This is why many Copilot companies cannot make the leap — it is not that the technology can't do it, but that the business model does not allow it.

This creates a structural opportunity for pure Autopilot startups: no legacy baggage, selling outcomes from day one.

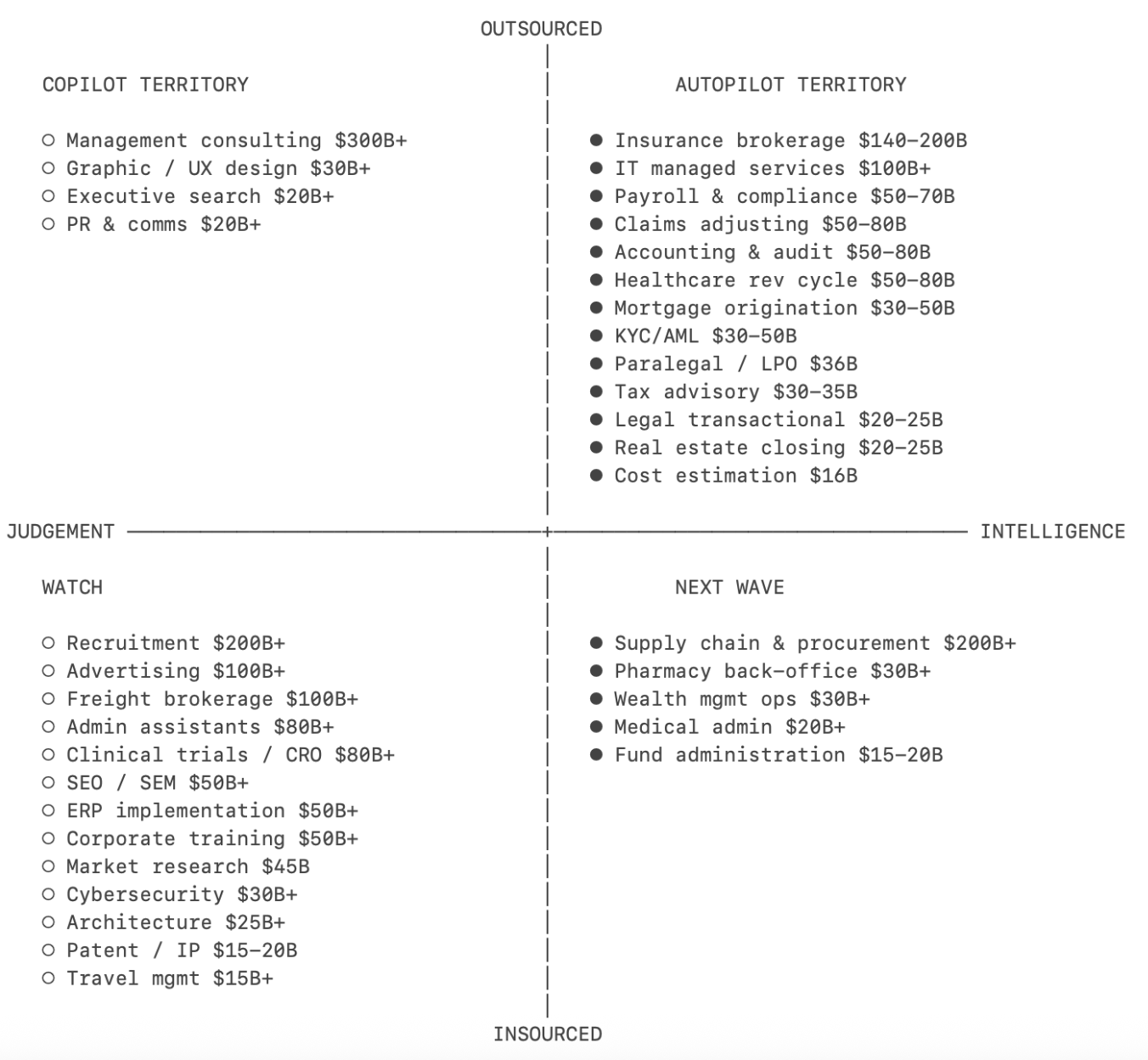

Ten Verticals Bek Named Specifically

The article lists specific TAM data and representative companies. Here are the key verticals:

| Vertical | Global Services TAM | Representative Companies | Model |

|---|---|---|---|

| Insurance Brokerage | $140-200B | WithCoverage, Harper | Direct insurance services |

| Accounting/Audit | $50-80B | Rillet, Basis | AI-generated financial statements |

| Healthcare Revenue Cycle | $50-80B | Anterior | Automated claims processing |

| Claims Adjustment | $50-80B | Pace, Strala | AI adjustment replacing manual |

| Tax Advisory | $30-35B | TaxGPT, Skalar | Automated tax filing |

| Legal (Transactional) | $20-25B | Harvey, Crosby | Automated contract review |

| Managed IT Services | $100B+ | Edra, Serval | AI operations |

| Supply Chain/Procurement | $200B+ | Magentic, AskLio, Tacto | Automated procurement comparison |

| Recruiting/Staffing | $200B+ | Juicebox, Mercor | AI recruiting |

| Management Consulting | $300-400B | High Judgement density, hard to enter | Human-AI collaboration |

Note the last row — management consulting has the largest TAM ($300-400B), but because it depends heavily on Judgement, it is currently the hardest to Autopilot. This does not mean it cannot be done — it simply requires a longer data accumulation cycle.

What Should Chinese Entrepreneurs Take Away?

Bek's article targets the Western market, but the core logic applies equally — or even more — to Chinese manufacturing entrepreneurs.

auto_awesomeChina's Manufacturing 1:6 Effect Is Even More Extreme

Chinese manufacturing enterprises may invest only a few hundred thousand yuan annually on ERP/MES and other software, but the human costs surrounding these systems — maintenance, data entry, report generation, quality inspection — can be 10-20x the software cost. This means the leverage from "selling tools" to "selling outcomes" is even greater in China.

Specific entry points for manufacturing AI:

Procurement Price Comparison — a classic Intelligence-dense task. Cross-comparing 3,000 supplier quotes, analyzing historical price trends, matching specification parameters — all rules. An AI Agent can complete in 12 minutes what takes 4 hours manually. Don't sell a comparison tool; directly deliver procurement recommendation reports.

Quality Anomaly Closed-Loop — from anomaly detection to root cause analysis to corrective action tracking, the process is fixed and the data is structured. Don't sell a quality inspection system; directly deliver quality closed-loop outcomes — AI-driven from anomaly discovery through resolution, with humans only confirming at critical nodes.

R&D Knowledge Management — structured retrieval and recommendations for material formulas, process parameters, and experiment records. Don't sell knowledge base software; directly answer R&D engineers' questions and provide formula recommendations.

The Four-Step Autopilot Startup Playbook

Bek provides a clear entry path in the article:

Start with Outsourced, Intelligence-Dense Tasks

Choose work that customers currently outsource to service providers (meaning this work does not require internal employees), and is primarily rule-based (Intelligence-dense), where AI can achieve 90%+ accuracy.

Deliver Outcomes with AI, Don't Sell Tools

Quote deliverables directly, not software licenses. Customers don't need to learn new tools, don't need training, don't need IT support.

Accumulate Domain Data, Build a Moat

Every delivery accumulates proprietary data — customer preferences, industry conventions, exception handling approaches. This data continuously improves your AI, and competitors cannot replicate it.

Gradually Encroach on the Judgement Domain

When the AI knows the industry well enough, start handling tasks that require judgement — not replacing humans, but democratizing judgement so small businesses can access the expert-level services that only large enterprises could previously afford.

A Signal Worth Watching

If a Sequoia Capital partner is publicly writing that "the next trillion-dollar company won't sell software but services," it means this thesis is no longer a hypothesis — it is happening now. The companies Sequoia is backing (Harvey, Rillet, Anterior, etc.) are already validating this model.

For Chinese AI entrepreneurs, the article's greatest value is not in copying Sequoia's homework — the US and Chinese markets differ too greatly. The value lies in a mindset shift:

Don't ask "what features does my AI product have?" Ask "what work can my AI help customers complete?"

The former makes you a tool company; the latter makes you a service company. In the AI era, service companies have a far higher ceiling than tool companies — because you are not eating the $1 of software, but the $6 of services.

This is precisely the positioning of FluxWise in the enterprise AI Agent space: not selling Agent platform licenses, but helping manufacturing enterprises directly deliver scenario-specific AI automation outcomes. From procurement comparison to quality closed-loop, from R&D knowledge to supply chain decision-making — selling outcomes, not tools.

Original source: Services: The New Software — Julien Bek, Sequoia Capital, March 5, 2026